Technocracy News & Trends has provided article after article, explaining tokenization. My new book, The New Economics of Technocracy: You Will Own Nothing, deals with it extensively. You must get your head around tokenization and understand that it will spell the end of private property, flipping us into an asset-based economic system just like Technocrats in the 1930s spelled out. Time is running out to send these grifters packing! ⁃ Patrick Wood. Editor.

In January, I published “The Tokenization of Everything.” The argument was not that blockchain is evil or that every tokenized asset is a control device. The argument was narrower and more dangerous: once property, money, credentials, and access rights are converted into programmable digital instruments inside a regulated, bank-integrated ecosystem, ownership quietly mutates into conditional permission.

Tokens are not neutral representations of property. They are code that can be designed to expire, freeze, restrict, or revoke based on compliance scores, policy triggers, or algorithmic rules set somewhere upstream. I named the legislative scaffolding — the GENIUS Act, the CLARITY Act — and the institutional cheerleaders, from BlackRock’s Larry Fink to then–Commerce Secretary Howard Lutnick. The warning was structural: a subscription society where durable property rights are replaced by revocable permissions, and where opting out becomes impractical because the rails of daily life run through the new system.

In February, I published “The Proof of Persona: Decoding Patent 060606.” That essay went one layer deeper. Microsoft’s published patent application WO2020060606A1 describes a cryptocurrency system in which a task is issued to a user device, a sensor captures body activity, the resulting data is transformed into a compact proof, and a cryptocurrency reward is issued if the proof satisfies validity conditions defined by the system. The patent publication explicitly contemplates that a user can solve the validation problem “unconsciously.”

The point was not that this system is currently deployed. The point was that someone considered it feasible enough to file: a published blueprint for moving the credential from what you do to what your body does — proof-of-work to proof-of-response to proof-of-compliance. I called it the hash of the soul, and I argued that the deepest battle is not technical but metaphysical: whether persons are real prior to systems, or whether personhood is a status conferred by what a validation server can read and certify.

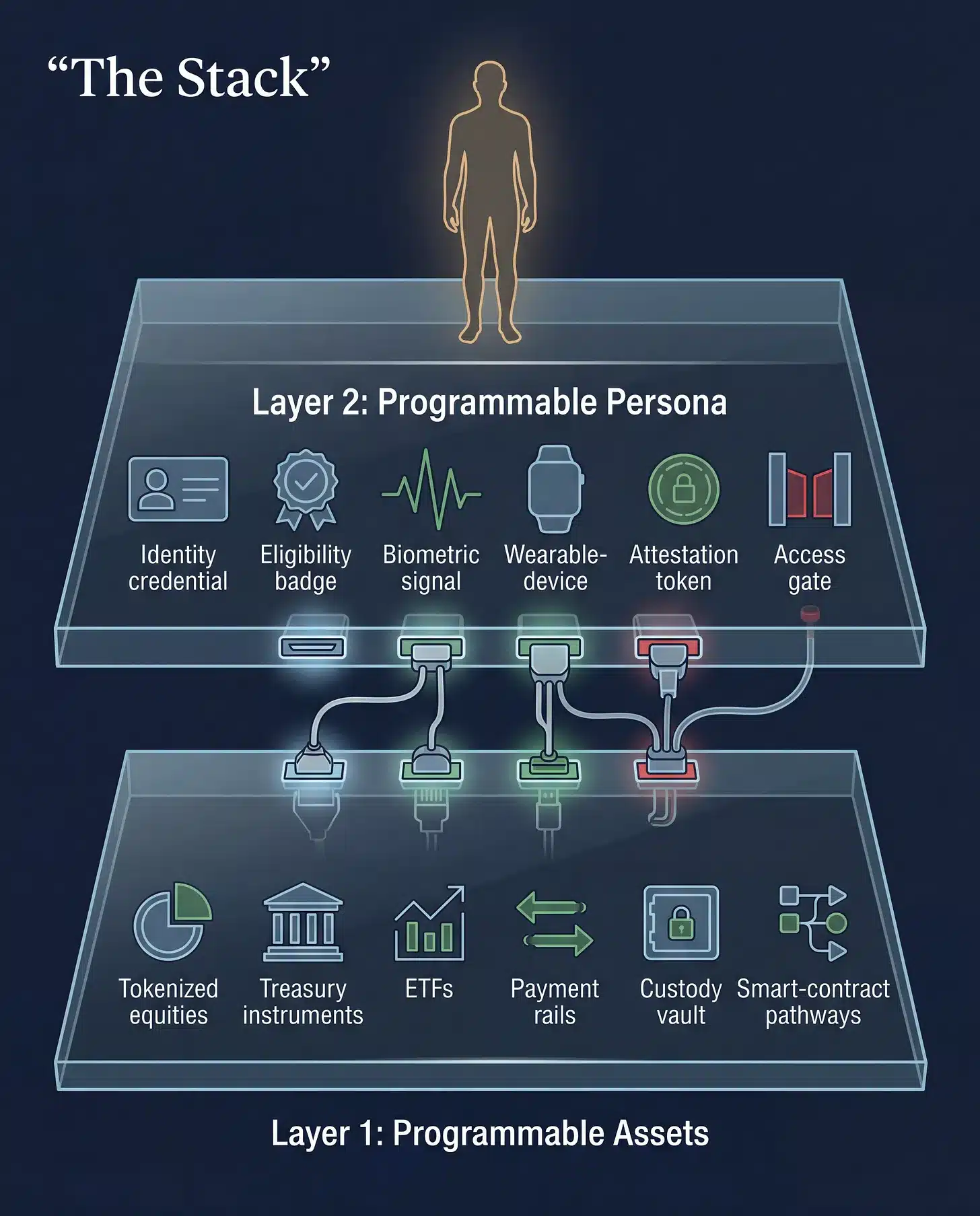

The two pieces, taken together, sketched a stack:

Layer 1 — Programmable assets. Property, money, securities, and services rendered into tokens that obey rules embedded by issuers, custodians, and regulators.

Layer 2 — Programmable persona. Identity, eligibility, attention, and eventually body-derived signals rendered into ledger-native attestations that condition access to Layer 1.

I argued that the danger of the stack is not in any single feature but in the convergence: a world in which both your assets and your standing are entries in a controlled ledger, and where the ledger doesn’t have to ask what you believe — only whether your wallet, your credential, or your body produced an acceptable profile.

That was the warning.

This is the rollout.

What DTCC Just Announced

On May 4, 2026, the Depository Trust & Clearing Corporation announced that its subsidiary, The Depository Trust Company, will facilitate initial, limited production trades of tokenized real-world securities in July 2026, with a planned full service launch in October 2026. The service has been developed with input from more than fifty financial industry firms. The published working group is not a marginal coalition. It is, in effect, the spine of the U.S. financial system plus the institutional crypto layer:

Major banks: J.P. Morgan, Goldman Sachs, Morgan Stanley, Bank of America, Citi, Wells Fargo, HSBC, BNP Paribas, UBS, State Street, BlackRock, RBC Capital Markets, TD Securities, Lloyds Bank.

Asset managers and clearing/custody: BlackRock, Franklin Templeton, Invesco, Charles Schwab, Apex Clearing, Broadridge, FIS, SEI, BetaNXT.

Market makers and brokerages: Citadel Securities, DRW, Virtu Financial, Jefferies, StoneX, Robinhood, TradeStation, Raymond James, Marex.

Crypto-native infrastructure: Circle (issuer of USDC), Anchorage Digital, BitGo Bank & Trust, Fireblocks, Ondo Finance, Ripple Prime, Payward (parent of Kraken), Digital Asset (creators of the Canton Network), Talos, Bitwave, Backpack.

The eligible assets are not fringe instruments. They are the bloodstream of U.S. capital markets:

Russell 1000 constituents (the largest U.S. publicly traded equities)

ETFs tracking major indices

U.S. Treasury bills, bonds, and notes

DTCC says The Depository Trust Company currently custodies more than $114 trillion in assets, and that DTCC’s subsidiaries collectively processed securities transactions valued at $4.7 quadrillion in 2025. The Federal Reserve identifies DTC as a central securities depository and securities settlement system, and lists it among the financial market utilities that the Financial Stability Oversight Council has designated as systemically important.

The service rests on a December 2025 SEC no-action letter authorizing DTC to offer a defined tokenization service for DTC Participants and their clients for three years, subject to representations and limitations. A no-action letter is not a statutory rewrite — the SEC staff explicitly noted that the response was based on the facts presented, did not necessarily endorse DTC’s legal conclusions, and could be modified or revoked. So the documented claim is not “the entire securities market is now tokenized.” The documented claim is this: the systemically important securities depository at the center of U.S. post-trade infrastructure has received regulatory cover to launch a regulated tokenization service for the most liquid assets in the country, and it has fifty of the world’s largest financial institutions in the working group.

That alone would be significant.

What makes it the rollout I warned about is the design.

“Same Rights” Wrapped Around a New Control Surface

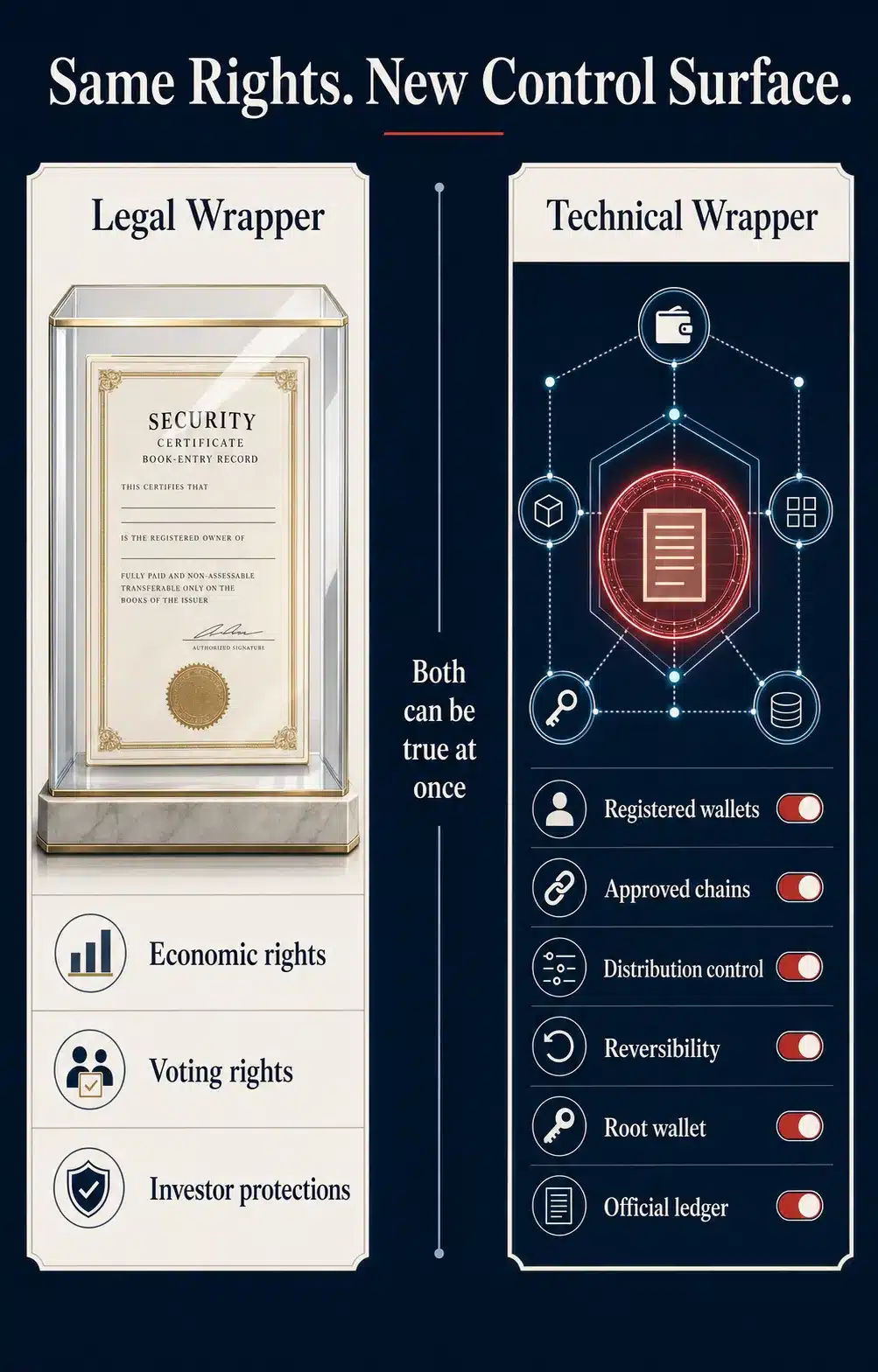

DTCC’s public framing emphasizes continuity. Tokenized assets, the company says, will carry the same legal and economic rights, investor protections, and ownership entitlements as the underlying securities held in traditional form.

This is not corporate spin, and it deserves to be stated at its strongest. The SEC no-action letter is explicit on the point. DTC’s request letter, which the SEC published as an attachment to the staff response, states that “a Tokenization Instruction would not change the legal framework governing the Participant’s holdings of the Subject Securities. The Participant would (until it transfers the Tokens) remain the entitlement holder with a security entitlement to the Subject Securities subject to the full suite of Article 8’s provisions and protections.” Corporate actions, including cash dividends, would be processed exactly as they are for traditional book-entry holdings. Whatever voting rights and economic entitlements the underlying Russell 1000 stock or ETF carries today, the tokenized version carries tomorrow.

That matters. It distinguishes DTCC’s service from the rights-stripping critique that gets aimed at certain crypto-native “tokenized equity” platforms. This is not a memecoin with a marketing deck. The legal entitlement to the underlying security survives tokenization in full.

So the institutional reassurance is real on its own terms. The question is whether legal-rights continuity is the right frame for evaluating what is actually being built.

But the architecture documented in the SEC’s December 11, 2025 no-action letter — and in the underlying request letter from DTC, which the SEC published as an attachment — tells a different story.

The no-action letter establishes the following as documented features of the program. DTC will retain a “root wallet” on each approved blockchain, with keys that, in the letter’s own language, allow DTC to “convert, transfer, mint, or burn any of the Tokens, even without the private key for the Registered Wallet.” DTC’s broader tokenization service materials describe an expanded set of administrative controls — including Clawback, Pause/Unpause, and Freeze/Unfreeze — implemented through compliance-aware token standards such as ERC 3643, which DTC explicitly names in the request letter as one of the protocols it has identified as compliance-aware. A monitoring system called LedgerScan — an off-chain, cloud-based DTCC software that resides in a public cloud and scans the underlying blockchains — will track token movements and Registered Wallet holdings in near real time. And the line that matters most, lifted verbatim from the no-action letter: “For purposes of recording Tokenization Entitlements, LedgerScan’s record would constitute DTC’s official books and records.“

To put the architecture plainly — this is my own paraphrase — what is being built is an asset that DTC can convert, transfer, mint, or burn at will through a root wallet; that can only move between wallets the institution has approved; on blockchains the institution has approved; under tokenization protocols the institution has certified as “compliance aware” with “distribution control” and “transaction reversibility”; whose movements are visible to DTC in near real time through an off-chain cloud system; whose official ownership record is not the public chain but DTC’s own LedgerScan ledger; and where every wallet permitted to hold the asset has been independently sanctions-screened by DTC against the Office of Foreign Assets Control list.

That is precisely the structure I described in Part I, now built into the official securities layer.

The legal wrapper says: same rights, same protections, same entitlements.

The technical wrapper says: programmable, reversible, freezable, and permissioned by design.

Both are true at once. That is the point.

The legal entitlement may remain intact while the technical wrapper introduces permissioning, reversibility, monitoring, and override authority.

The Compliance-Aware Protocol Is the Chokepoint

The SEC no-action letter is more revealing than the press release.

According to the staff letter, any DTC Participant wishing to use the tokenization service must register one or more blockchain addresses as a Registered Wallet on an approved network. Tokens may be transferred only between Registered Wallets. DTC determines which blockchains are approved, which protocols are acceptable, and which standards are supported.

Most importantly, in order for DTC to support a tokenization protocol, DTC must determine that the protocol is “compliance aware” — and the letter defines what that means with admirable clarity. A compliance-aware protocol must support distribution control (preventing the token from moving to any address that is not a Registered Wallet) and transaction reversibility (allowing DTC to force-convert or transfer the token using a “root wallet” when conditions warrant reversal).

Translate that out of regulatory English:

The asset can only travel inside the approved perimeter.

The protocol must structurally prevent the asset from leaving the perimeter.

The institution retains a root key that can override the chain.

Reversal is a feature, not a bug.

Every wallet authorized to operate is independently sanctions-screened by DTC against the Office of Foreign Assets Control list before it is permitted to participate.

The no-action letter also states verbatim: “At all times, the registered ownership of the Subject Securities represented by a Tokenized Entitlement would not change; the Subject Securities would remain registered in the name of Cede & Co., DTC’s nominee.” Tokenization is not an escape from the existing indirect-holding system. It is a new digital representation inside that system, with new control affordances bolted on.

This is the architecture in operational form. The token is not a sovereign bearer asset in the romantic crypto sense. It is a tokenized entitlement, tied to a custodied security, held in an approved wallet, on an approved chain, under a compliance-aware protocol, recorded on an institutional ledger that constitutes the official record.

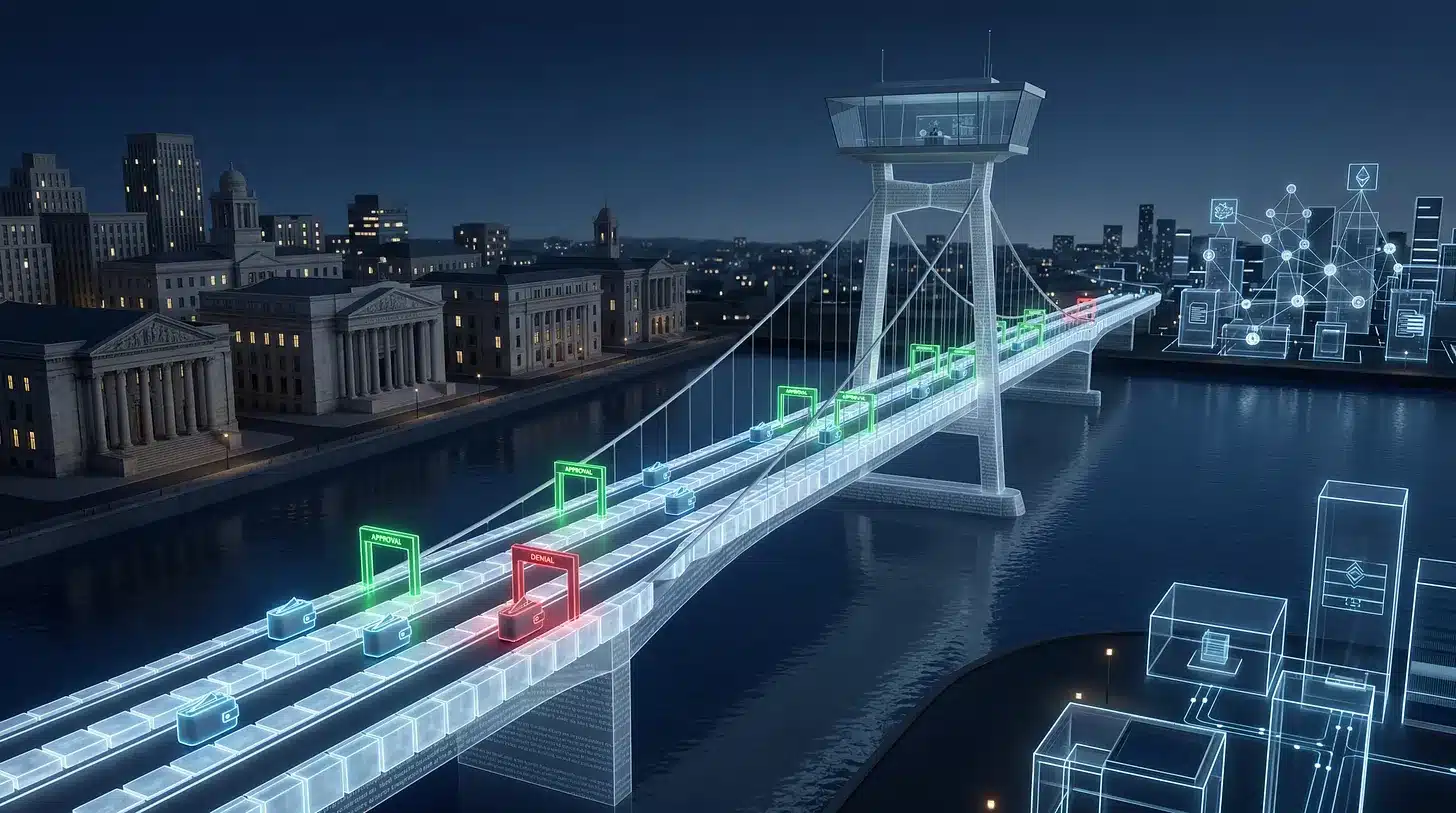

The polite name for this is “bridge between TradFi and DeFi.” That is DTCC’s own phrase. But a bridge is not neutral when all traffic must pass through controlled lanes. A bridge can connect. It can also filter, toll, audit, reverse, freeze, and exclude. The infrastructure choice is the political choice. Once the bridge is the only path, the bridge-keeper is the sovereign.

A bridge can connect two systems. It can also decide which traffic is allowed to cross.

This Is What I Meant by “Conditional Access”

In Part I, I argued that the deep danger of tokenization is the conversion of ownership into access — possession into a system-recognized entitlement. Critics suggested I was extrapolating beyond the evidence. As of May 4, the extrapolation has documentation.

Consider what DTCC’s design actually says about the future of “ownership”:

Your equity position exists as a token in a Registered Wallet, not in your name.

Movement of that token is restricted to other Registered Wallets, by protocol.

A monitoring system tracks every transfer in near real time.

The institution can pause, freeze, claw back, or force-transfer the token if conditions defined upstream are met.

The official record of who owns what is not the chain — it is the institution’s ledger system.

The legal entitlement is preserved, but its exercise depends entirely on the system’s recognition of your wallet, your protocol, and your standing.

The public chain may show movement, but the official record belongs to the institution that recognizes the entitlement.

That is the textbook definition of conditional access. The asset is yours — until it isn’t. The token moves — until it doesn’t. The chain is open — except where it isn’t.

This is not yet a Chinese-style social credit overlay on U.S. capital markets, and I am not claiming it is. There is no public evidence that DTCC is currently linking securities ownership to political behavior, vaccination status, ESG scores, or biometric attestations. What I am claiming is narrower and therefore stronger: the architecture now contains every mechanism that such an overlay would require. Approved chains. Approved wallets. Compliance-aware protocols. Reversibility. Root-wallet override. Near-real-time surveillance. An official institutional record that supersedes the public ledger.

The features may be defended as fraud prevention, error correction, sanctions compliance, and recovery. Of course they will be. That is exactly how technocracy is sold — not as control, but as protection. Not as a coup, but as an upgrade. As one commenter on Part II put it: like a thief in the night.

The civil-liberties question is not whether a compliance rationale exists. The question is what happens when ownership itself becomes inseparable from a programmable compliance envelope, and when the envelope is operated by a single systemically important utility at the center of the world’s largest capital market.

Where DTCC Closes Loop 1 — and Prepares the Rail for Loop 2

This is where the third installment must do work the first two could not.

In Part I, I described the asset layer. In Part II, I described the persona layer — soulbound tokens, ledger-native attestations, biometric and physiological proofs that turn identity, reputation, and eventually body activity into on-chain credentials. The two layers were treated as parallel. They are not parallel. They are sequential.

Programmable assets are useless without a credential layer that decides who may hold them.

Today, DTCC’s “credential layer” is institutional: a wallet is registered because a DTC Participant — a regulated bank, broker, or custodian — vouches for it under existing KYC/AML obligations. That is the conventional gate. But once Registered Wallets become the only legitimate carriers of tokenized stocks, ETFs, and Treasuries, the question of what attestations a wallet must satisfy to be eligible becomes the entire game.

It is a short logical step from:

“This wallet is registered because a DTC Participant verified the holder’s identity under KYC.”

to:

“This wallet is registered because the holder has presented attestations of identity, residency, accreditation, sanctions standing, and tax status.”

to:

“This wallet is registered because the holder has presented ledger-native, soulbound, or body-derived attestations satisfying the system’s eligibility schema.”

Each step is sold as a security or compliance upgrade. None of them require a single new statute. They require only that the existing rail — Registered Wallets, approved chains, compliance-aware protocols — be extended to accept richer credentials over time. The credentials that Part II warned about are precisely the kind of attestations that would slot naturally into a Registered Wallet model.

Layer 1 controls the asset. Layer 2 decides who is eligible to touch it.

I am not claiming this integration is happening today. I am claiming the rail is now built such that it can. That is the difference between speculation and rollout. Speculation says: this could happen. Rollout says: the institutional infrastructure required for it to happen has been authorized, scheduled, and resourced, with fifty of the world’s largest financial firms in the working group and a Wall Street clearinghouse running point.

Once Layer 1 is live, Layer 2 has somewhere to plug in.

The Internet of Bodies Has a Settlement Layer Now

In Part II, I cited RAND’s work on the Internet of Bodies — the growing class of devices that monitor human physiology, transmit data over networks, and collect personal information whose ownership and governance remain unsettled. I cited the engineering literature on the Internet of Bio-Nano Things. I cited the OpenAI/Jony Ive hardware vector and HHS Secretary Kennedy’s stated goal of universal wearable adoption within four years. I cited TESCREAL and the Santa Fe Institute’s “engineering crypto-economies” work, with Thiel-foundation patronage in the background. The argument was that the body is being progressively wired as the next interface layer, and that “participation” is migrating from clicks toward physiological signatures.

Without a programmable financial settlement layer, all of that biometric infrastructure is just data extraction.

With one, it becomes governance.

DTCC has now announced the settlement layer.

I want to be precise: DTCC is not building the Internet of Bodies. DTCC is not implementing Microsoft’s WO2020060606A1. DTCC is not collecting biometric data. The connection I am drawing is architectural, not corporate. It is the same connection I drew in Part I about money and assets, and in Part II about identity and physiology: modern systems are not built as isolated silos. They are built as stacks. A programmable financial substrate, an emerging biometric credential layer, AI-mediated risk scoring, and ledger-native attestations do not have to share a corporate parent to become mutually reinforcing. They only have to share interface standards.

DTCC’s tokenization service introduces those standards into the official financial core. Approved chains. Approved wallets. Compliance-aware protocols. An institutional ledger of record. The rest of the stack is being assembled in parallel — by other firms, in other industries, under other regulators — and the interfaces are converging.

The Internet of Bodies, in other words, now has a place to settle.

Body-derived data becomes governance only when it can be connected to access, eligibility, and settlement.

What This Does Not Prove

Because the temptation in this terrain is to overshoot, let me be explicit about the boundary between evidence, interpretation, and projection.

What the evidence shows:

DTCC’s announcement of a tokenization service for DTC-custodied securities, with limited production in July 2026 and a planned launch in October 2026.

A working group of more than fifty firms, including the largest U.S. banks, asset managers, market makers, brokerages, exchanges, and crypto-native infrastructure providers — published by name in DTCC’s release.

An eligible asset set covering Russell 1000 constituents, major-index ETFs, and U.S. Treasuries.

An SEC staff no-action letter, issued December 11, 2025, authorizing the service for three years under defined conditions.

DTC’s retained authority via a “root wallet” on each approved blockchain, with keys that — in the no-action letter’s own language — allow DTC to “convert, transfer, mint, or burn any of the Tokens, even without the private key for the Registered Wallet.” DTCC’s tokenization service materials describe an expanded set of administrative controls (Clawback, Pause/Unpause, Freeze/Unfreeze) implemented through compliance-aware token standards such as ERC 3643, which DTC explicitly names in the request letter.

Registered Wallets, approved blockchains, “compliance aware” tokenization protocols with documented “distribution control” and “transaction reversibility” requirements (terms used verbatim in DTC’s request letter).

Independent OFAC sanctions screening by DTC on every Registered Wallet before it is permitted to operate.

Near-real-time surveillance of token movements via LedgerScan, an off-chain DTCC software system residing in a public cloud, whose record constitutes DTC’s official books and records.

Continued registration of underlying securities in the name of Cede & Co., DTC’s nominee.

What the evidence does not prove:

That every U.S. security will be tokenized.

That DTCC is presently linking securities ownership to social credit, vaccine status, carbon scores, biometric verification, or political compliance.

That Microsoft’s WO2020060606A1 has been deployed or integrated with any market infrastructure. (Google Patents currently lists the WO publication’s legal status is listed as ‘ceased’ on Google Patents (a reflection of PCT international-stage expiration, not necessarily abandonment of the underlying invention).

That the July 2026 limited production trades will themselves transform the market.

That any individual firm in the working group is pursuing the architectural extensions I have described.

What I am interpreting:

That the design choices documented above — taken together, in the institution that sits at the center of U.S. post-trade infrastructure — constitute the operational rollout of the asset layer I described in Part I, and the rail-laying for the persona layer I described in Part II.

That this is the moment when “tokenization of everything” stops being a thesis at the speculative edge of crypto and becomes part of the official market plumbing.

That the public framing of the project (”same rights,” “investor protection,” “operational efficiency”) is functioning, whether by design or by drift, as a normalization mechanism for programmable compliance.

That is enough to warrant scrutiny. It does not require maximalist claims to be alarming.

The Polite Language of Enclosure

The rollout will not be sold as control. It will be sold as efficiency, liquidity, transparency, investor protection, fraud prevention, security, interoperability, and modernization. DTCC’s own materials describe the service in those terms, and some of those benefits may be genuine. That is precisely why the rollout is powerful.

Control systems that offer no convenience are easy to refuse. Control systems that offer 24/7 settlement, fractionalization, automation, capital efficiency, and access to new financial services are adopted voluntarily until opting out becomes impractical. Then they are adopted by institutional momentum. Then they become required for ordinary participation in markets, retirement accounts, payrolls, mortgages, and brokerage relationships. Then the question of whether you “consent” to programmable, freezable, reversible ownership becomes academic, because the alternative has been quietly retired.

This is the lesson Part I tried to surface and Part II tried to deepen: the cage is not built by coercion. It is built by dependency. Programmable infrastructure does not need to be tyrannical to make tyranny technically easy, administratively elegant, and rhetorically defensible. The control surface is the point. The control surface is what the public does not see, because the public is told to look at the rights, the protections, the entitlements, the modernization, the convenience.

The control surface is what I have been writing about for two articles.

It now has a launch date.

The Question Hiding Inside the Technical One

The argument over tokenization is usually framed as engineering: blockchain versus databases, settlement speed, smart contracts, market modernization. Beneath the engineering is a political question, and beneath the political question is a metaphysical one — the same one I named in Part II.

Do persons exist prior to the system, or are persons constituted by it?

Does property precede the ledger, or does the ledger confer property?

Are rights inherent in the human person, or are they permissions issued by a validation regime that decides which wallets, which credentials, and which signatures qualify?

The Declaration of Independence has an answer. Its argument presupposes an order of being that political power does not manufacture: persons are real in themselves, dignity is intrinsic, rights are not granted by the state. A realist metaphysics of this kind is the one ground on which programmable enclosure can be refused, because it insists on a layer of reality the system cannot author.

The opposing view — the one quietly encoded into every “compliance-aware” protocol, every soulbound credential schema, every body-derived proof system — is that the human person is a pattern emerging from sub-personal variables, that the measurable is the most real, and that the most real is the most governable. Under that story, the validation server is not pretending to confer standing. It is simply registering it. Personhood becomes an attestation. Property becomes an entry. Standing becomes a permission.

DTCC’s tokenization service does not, by itself, settle that question.

But it operationalizes the answer that one side of the question prefers.

The Architecture Is Not Yet Closed

The rollout is scheduled, but it is not finished. The SEC no-action letter expires in three years and, in the letter’s own language, “is subject to modification or revocation by the Staff at any time.” Production trades do not begin until July. The full launch is not until October. Every interface in the stack — the approved-chain list, the certified protocols, the wallet credential schema, the compliance-aware standards — is still being defined. None of this is locked in yet. The architecture is being built, but the design space is still open.

That is where the leverage is.

The SEC no-action letter itself. The relief is not a statute. It is staff discretion, granted under defined representations, subject to modification or revocation. Public comment to the Division of Trading and Markets and to the Commission’s public comment channels is the most direct lever there is. As of this writing, the SEC has only three sitting commissioners — Chair Paul Atkins, Hester Peirce, and Mark Uyeda, all Republicans — following Caroline Crenshaw’s departure in January 2026, which left both Democratic seats vacant. The dissenting voice that historically pushed back on architectures like this one is no longer at the table. That makes public pressure on the remaining commissioners, on whoever is eventually nominated to fill the open Democratic seats, and on the Division of Trading and Markets staff who issued the no-action letter, more important rather than less. Comments anchored in the technical architecture — root-wallet authority, force-transfer, LedgerScan as the official record, OFAC screening of every wallet — will carry more weight than generic anti-crypto sentiment, because the architectural concerns are the genuinely novel ones the Staff has not publicly reckoned with.

And I have watched this work firsthand. In late 2023, I sounded the alarm across multiple shows — including Infowars — about the NYSE’s proposed rule (SR-NYSE-2023-09) to list Natural Asset Companies, a vehicle that would have allowed private capital, including foreign-controlled sovereign wealth funds, to monetize “ecosystem services” on American public, private, and tribal land. The day after one such appearance, the NYSE withdrew the proposal. It was not me alone — thirty state financial officers had filed a comment letter, the House Natural Resources Committee had opened a probe, and a broad coalition had been organizing for months — but it was a coordinated public-pressure campaign that succeeded, and I had a documented role in it. The withdrawal landed on January 17, 2024, the day before the extended comment deadline closed. The proposal does not exist today because the public showed up. The same window is open here.

Congressional oversight of systemically important utilities. DTC was designated a SIFMU under Title VIII of Dodd-Frank, which carries oversight authority through the Senate Banking and House Financial Services committees. The members who voted for the GENIUS and CLARITY Acts are now on the hook for the downstream architecture those bills enabled. Hearings can be demanded. Documents can be requested. The specific carve-outs from Section 17A of the Exchange Act, Reg SCI, and Rule 19b-4 that the no-action letter grants — the rule-filing exemption, the Reg SCI exemption, the Rule 17ad-25 exemption — can be scrutinized in public, which is precisely the scrutiny the no-action mechanism was designed to avoid.

State law is still operative. This is the leverage point most people miss. Article 8 of the Uniform Commercial Code — which the no-action letter explicitly relies on as the bedrock of the participant’s preserved entitlement — is state law, not federal. DTC is a New York limited purpose trust company. State legislatures, particularly Delaware (where most public corporations are domiciled), Texas, and Florida (which have been actively legislating on property-rights and anti-CBDC frameworks), can pass clarifying statutes — for example, requiring that any force-transfer of a securities entitlement occur only by court order, or that a non-programmable book-entry alternative be permanently maintained for any tokenized security. New York DFS has direct jurisdiction over DTC’s trust status. Federal preemption arguments are real, but they are far from absolute on questions of property law, fiduciary duty, and consumer protection.

Issuer pushback. The Russell 1000 companies whose shares are about to be wrapped in programmable, freezable, force-transferable tokens have not been asked. They are the issuers. They have shareholder relationships, transfer agent contracts, and board fiduciary duties that arguably should weigh whether their securities get folded into a permissioned compliance envelope — even if the underlying legal entitlement is preserved. A handful of CEO or board statements requesting carve-outs, or demanding plain-English disclosure to retail shareholders before any of their stock is tokenized, would change the politics quickly. Shareholder proposals submitted under SEC Rule 14a-8, paired with vote recommendations from the dominant proxy advisors (ISS and Glass Lewis), are the formal vehicle for putting tokenization eligibility in front of the board on the annual ballot.

Participant opt-out. The service is voluntary at the DTC Participant level. Charles Schwab, Robinhood, Fidelity, Vanguard, and every other broker-dealer and custodian on the working group roster choose whether to register wallets and route client securities through them. Each one can also commit to maintaining a permanent non-tokenized custody option for retail customers who want one. Direct pressure on the firms whose brand identity is built on retail empowerment is the fastest market-based lever available, and it does not require any regulator to act first.

The intellectual fight. Every line of code in this stack is being written by humans who answer to professional and reputational incentives. Sustained, serious, fact-based critique — the kind that lands on the desks of the lawyers writing request letters, the engineers writing protocol standards, and the commissioners voting on relief — changes the design space within which the next iteration is built. Most of the choices in this rollout were made under the assumption that the public would not notice the difference between “same rights” and “programmable rights.” That assumption is the soft underbelly.

What I would not bet on is the idea that a parallel decentralized system will simply route around all of this. The regulatory framework being built — the OFAC-screened wallet model, the compliance-aware protocol requirement, the GENIUS and CLARITY rails for stablecoins and tokenized deposits — is specifically engineered to narrow the parallel system over time, not enlarge it. The fight is not at the edges of the system. It is at the center, before the center hardens.

There is a deadline. The first production trades begin in July. Every leverage point above is exercised before the architecture sets, or it is exercised against an architecture that is already running. The window is open. It will not stay open indefinitely.

Conclusion: The Ledger Is Becoming the Law

The central issue is not blockchain. It never was. The central issue is whether the architecture of ownership — and eventually of personhood — is being rebuilt around programmable compliance, with control surfaces concentrated in institutions that the public neither elected nor effectively oversees.

DTCC’s announcement shows the institutional layer of that rebuild moving from concept to schedule. The systemically important depository at the center of U.S. capital markets, with $114 trillion in custody and a working group spanning the largest banks, asset managers, market makers, and crypto-native infrastructure providers in the world, is preparing to support tokenized entitlements, registered wallets, approved chains, near-real-time surveillance, compliance-aware protocols, and reversible token controls under the legal framing of “same rights, same protections.”

That is not a conspiracy theory. That is the documented architecture, as published by DTCC and as authorized by the SEC’s December 2025 no-action letter.

The interpretation is mine, and I will own it: this is the institutional rollout of the asset layer I warned about in “The Tokenization of Everything,” and it is the rail on which the persona layer described in “The Proof of Persona” will eventually run. Neither piece of the stack is fully assembled. Both are being built. The question is no longer whether tokenization is coming, but who is writing the rules of the tokenized world — and whether human beings retain rights inside it, or merely permissions.

Once ownership is programmable, the fight is no longer over markets.

It is over sovereignty.

It is over what a person is.

It is over whether the ledger can rightfully become the referee of standing — or whether there remains, behind every measurement and every attestation, a human being who is real before the system reads them.

Patrick Wood is a leading and critical expert on Sustainable Development, Green Economy, Agenda 21, 2030 Agenda and historic Technocracy. He is the author of Technocracy Rising: The Trojan Horse of Global Transformation (2015) and co-author of Trilaterals Over Washington, Volumes I and II (1978-1980) with the late Antony C. Sutton.